How to Boost Your Portfolio Yield Like A Pro

While stocks have made a comeback the past few months, one issue still faces investors: how to derive a steady yield from their portfolios. With Treasury rates at 1%, an investor with $3 million in retirement funds could only be certain of $30,000/annum in income; less than the average food server makes. The Fed has said to expect near zero rates through 2022 and a checking account earns even less. This means that dividends combined with tax minimization strategies should be the focus of most investors’ portfolios right now.

The total return is capital appreciation plus the dividend payout. Typically, the S&P 500 dividend payout is around 2% and it is currently at 1.80%. This is low, but higher than Treasury yields, which are below 1%. Those dividends matter! Over the past decade, a holder of the S&P 500 gained 188% without dividends. Adding in the 2%/annum yield and that return boosts by another 62% totaling up to a 250% return.

These are five strategies we use when thinking about boosting post tax income for our clients:

1. Focus on Dividend Growth Not Size

Early in the Covid-19 crisis, investors worried that dividend cuts were coming. Firms like Disney, Marriott and Ford did cut; however, things were not as bad as we expected. 13.10% of the companies in the S&P 500 have suspended or cut dividends, leaving 86% intact. Additionally, in the US, dividend cuts happened in industries that we could have predicted: energy, travel, and leisure; it has also been more along mid and small cap companies. So, the expected wave never occurred.

42.20% of S&P 500 companies have actually raised their dividends including Johnson & Johnson, Costco, and Procter & Gamble; this means for every 1 company that cut, more than 3 have increased their dividends.

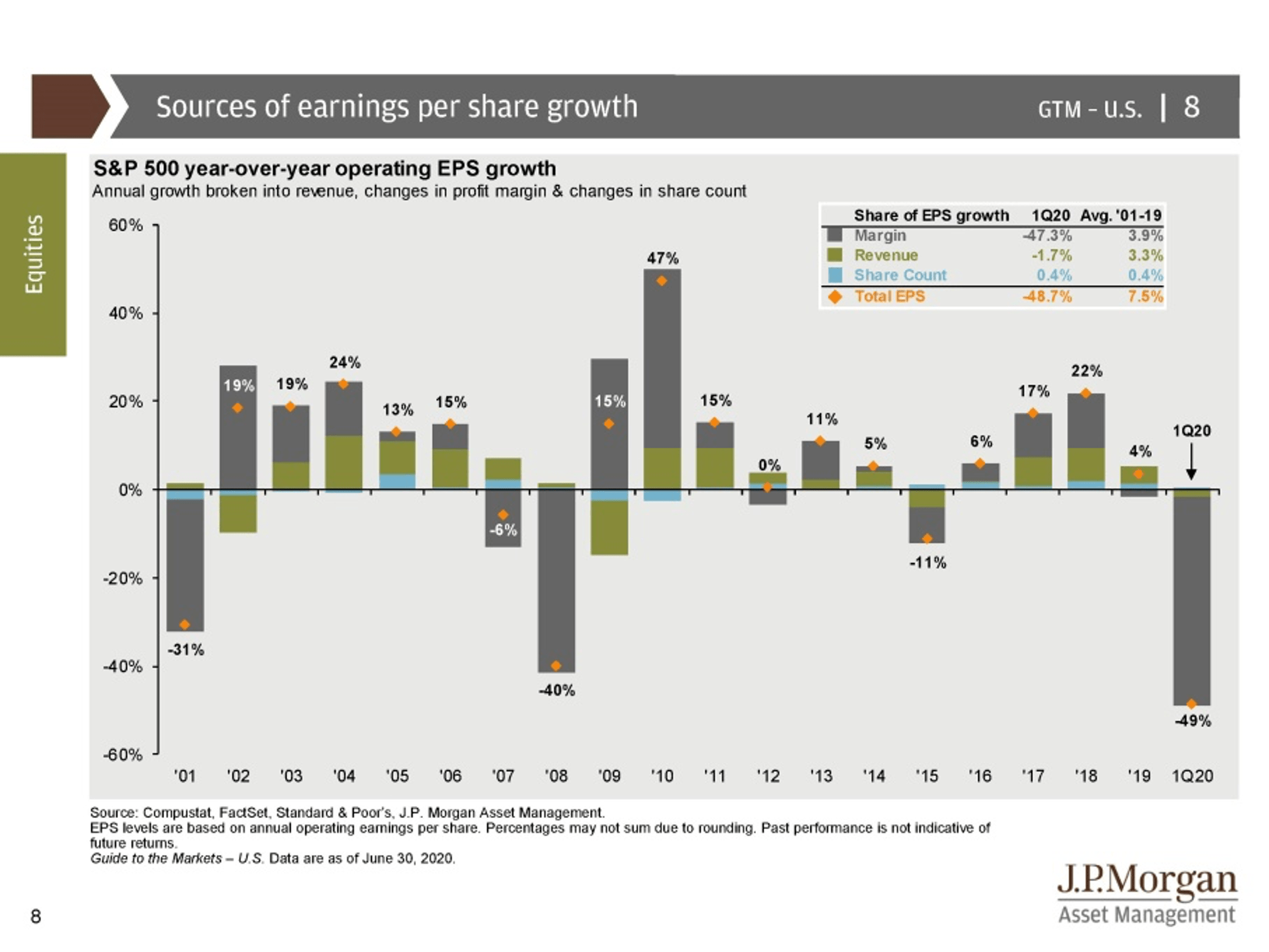

Interestingly, technology firms now pay 17% of the dividends paid in the S&P 500 which has risen from 5% in 2005. The old philosophy that growth stocks are the opposite of value stocks does not seem to be true in our current situation. Now we are seeing, the sector leading in growth is also leading in income.

2. Be A Politically Conscious Investor

Currently Joseph Biden leads in the polls. One point of concern for Democratic voters is executive compensation and corporate share buybacks. Therefore, there is a good chance that Biden winning the election would result in restrictions on share buybacks.

What is a buyback?

There are two ways for a corporation to return earnings to shareholders: buybacks and dividends. Buybacks have been very popular in recent years. Buybacks mean fewer outstanding shares, so each shareholder gets a higher percentage of each dollar earned.

The problem is that buybacks also cause executive stock options to rise in price which is a big source of the narrative about executive compensation becoming excessive relative to workers who get few if any stock options. As the political winds shift more towards social justice, we expect share buybacks to become increasingly untenable for corporations especially when they are often caught asking the government for favorable legislation or direct financial aid. Consequently, corporations will find increasing their dividend payout to be more sustainable and acceptable to their stakeholders. McDonalds is an example of a company that ended share buybacks but still pays a dividend. This is also true of the 8 largest banks.

If buybacks go away but corporations still want to return free cash to their shareholders, it is likely they will do it by an increase in dividends. Currently, investors have earned 2.30% on buybacks which is greater than the 1.80% return to dividends. Might this relationship invert, resulting in higher income to investors? Now is a good time for investors to purchase shares that have lower dividend yield priced into them. This acts as a defensive measure to protect one’s participation in the rise of the market and as an offensive measure to position oneself for future gains.

3. Be a Tax Savvy Investor

Another factor investors should consider is that Biden will propose an increase to the capital gains tax rate, equaling the ordinary income tax rate. In this way we expect dividends will become more favorable relative to growth investing—which has been favored for the past decade.

There are many dividend focused funds, but these could be problematic for retirees because of tax.

Normally, we expect to get taxed once on our dividends. But dividend funds usually generate extra taxable capital gains—which are out of the investor’s control. This would be fine if all fund holders got to realize the gain but, paradoxically they get none of it. Only those who sold out derive the benefit. So, this may not be the most tax savvy way to access good dividend paying stocks.

For example, look at the Fidelity Equity Income Fund. Seemingly the 1.97% dividend yield tracks the S&P 500. However, you ALSO pay tax on the .57% capital gain distribution at a 30% federal and state tax rate. This lowers the dividend yield to 1.80%; adding in the expense ratio, the dividend yield becomes lower than the S&P 500’s.

ETFs are better but in a perfect world, you would hold these types of income heavy securities in your retirement account. Then, parsing the growth aspects of your portfolio into your taxable account; where it can take advantage of lower capital gains tax treatment as well as tax loss harvesting to reduce your bill—did you tax loss harvest during the Covid-19 downturn?

4. Asset Location Matters

This brings us to how you hold onto your hard-earned income through asset location.

While pushing money into retirement plans is a good first measure, investors should also make efficient use of tax-free vehicles including 529 plans and more importantly, the Roth IRA.

A Roth conversion analysis is complex and varies with the particulars of the investor’s circumstance. We begin with an analysis, figuring out if it makes sense for the client. If so, we help our clients convert the funds, receiving the benefits of this very potent strategy.

5. Tax Efficiency Extends to Fixed Income Investing

All portfolios should have some bonds. Given that tax rates are going to rise on all types of income we want to focus on post tax savings. This comes in two forms: retirement account utilization and municipal bonds.

The Covid-19 crisis put state and local governments under intense pressure because no one is working, causing their income tax receipts to compress. Sales tax receipts are also low because businesses are seeing less product turnover. Yet the need for local government leadership and stabilization has never been more important—especially with the federal government placing responsibility on local governments to solve their Covid-19 problems.

The safety valve for local government is going to be the debt market, allowing them to borrow money and pay these liabilities. The problem is that local governments are currently under pressure on their credit, meaning a higher yield for investors. This could create an opportunity for good tax-free income if investors find good credits and participate while yields are high.

At Camelotta Advisors, we do a fixed income analysis to find situations most advantageous for our clients. As opposed to a mutual fund, we pick bonds that are suitable for each client’s individual circumstance. This high degree of tailoring is only available in a professionally managed investment context. Most retail investors have access to plenty of stocks, but do not have access to the universe of municipal bonds or the ability to analyze them as we do.

About Camelotta Advisors

Becoming rich is not about doing a million different things. It’s about focusing on a few things and doing them right. For almost 20 years we have helped successful people accomplish sustained wealth. Based in San Francisco and Seattle, we are a fiduciary working with a small number of select clients delivering highly tailored professional financial planning and portfolio management.

Get in Touch

You can send us an email or schedule a phone call with your team by using the calendar provided here.

Camelotta Advisors is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Camelotta Advisors and its representatives are properly licensed or exempt from licensure. This website is solely for informational purposes. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Camelotta Advisors unless a client service agreement is in place.